How Buyer Interest During Sell Pressure Is Signaling Strength in Crypto Markets

The market resilience this week of relatively high selling pressure should embolden medium- and long-term bulls.

Crypto remained under pressure over the past week due to short-term concerns over how potential releases by Mt. Gox and the German government could impact market price action. However, a cool June CPI print, which raised the market odds of an interest rate cut in September to 89% from 73% yesterday and 53% a month ago, lifted risk assets and paired losses over the week.

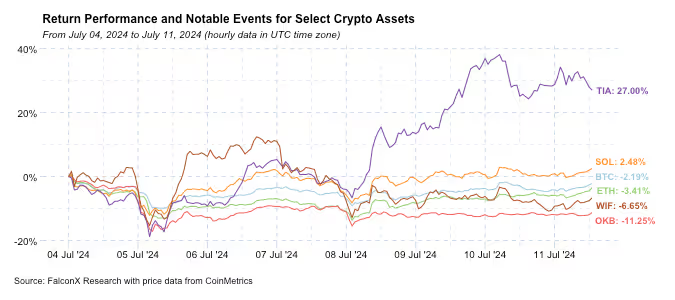

ETH and BTC continue to trade somewhat in tandem, with the ETH/BTC price ratio hovering around the 0.055 level, while SOL outperformed both majors. TIA recorded gains of almost 30% over the week despite a lack of clear news flow and funding rates in deep negative territory. Conversely, WIF and OKB continued to perform poorly and led losses among assets with a circulating market capitalization above $1 billion.

This week, the German government executed almost all of the sale of over 50,000 BTC (worth about $2.9 billion at current prices) seized in 2013 from the now-defunct piracy website Movie2K. According to on-chain data from Arkham Intelligence, the bulk of these sales took place over the past three days, and at the time this report goes to press, their holdings amount to only 4,925 BTC (or about $286 million at current prices).

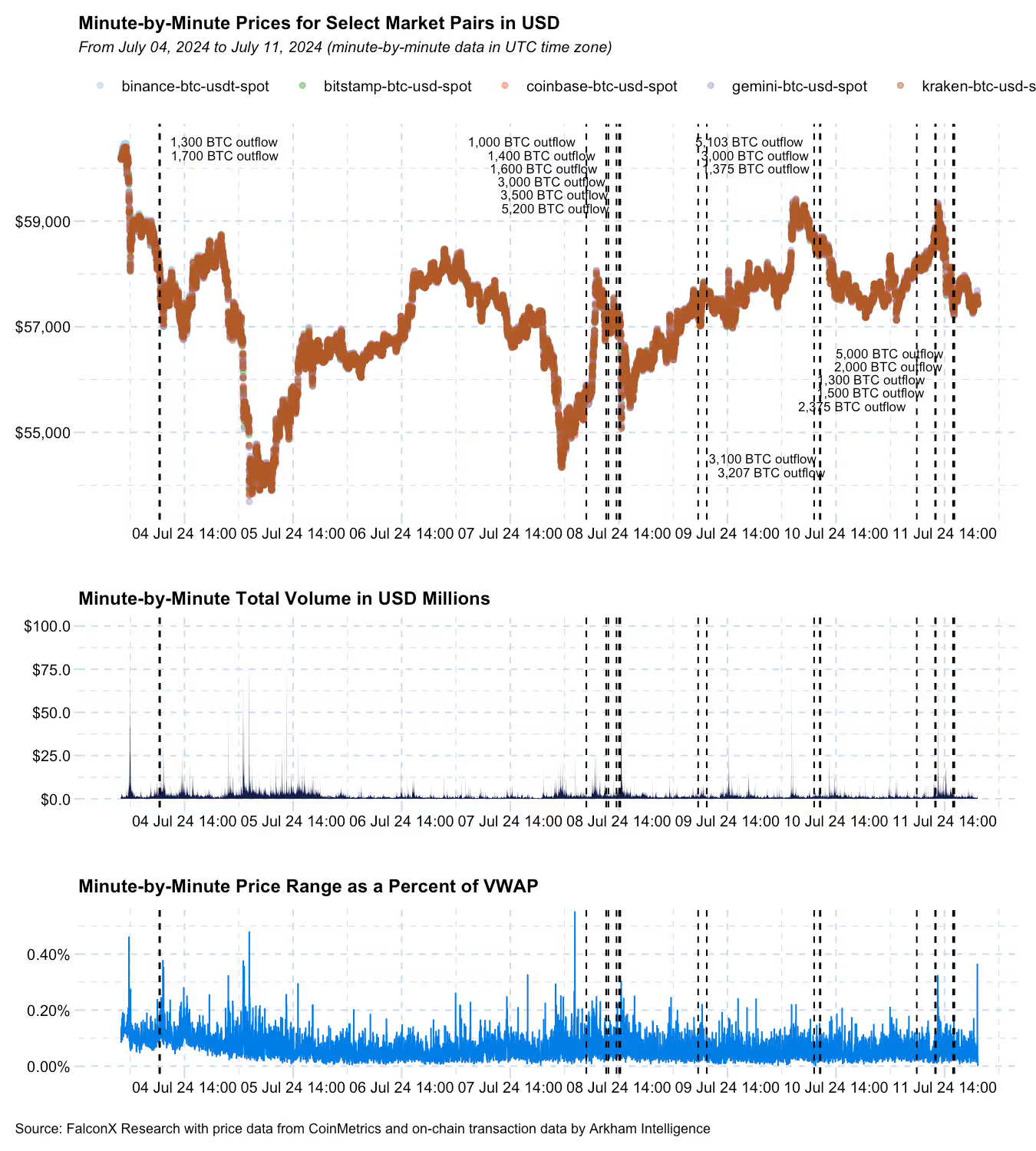

The charts below show the minute-by-minute price action of the leading spot BTC pairs (with the net on-chain outflows above 1,000 BTC highlighted), total volumes, and price dispersion across exchanges.

The steeper part of last week’s market correction took place on July 4th, likely due to Mt. Gox reportedly moving large amounts of BTC across wallets and a fair amount of liquidations exacerbating the price drop to below the $54k mark (more on that below).

However, the bulk of the sales from the German Government, representing almost 35,000 BTC, took place between July 8 and July 11 and had a remarkably low impact on prices. During this period, on-chain transactions indicate the sale of 12,365 BTC, 3,496 BTC, 8,411 BTC, and 10,636 BTC each day.

Although the market price took a hit after each group of transactions, it was also able to recover relatively quickly by the time the next batch of transactions hit the tape.

Significant buy demand showed up to cushion the price action.

For example, U.S. spot Bitcoin ETFs saw net inflows of $738 million between July 8 and July 11, despite ongoing selling pressure and intraday volatility.

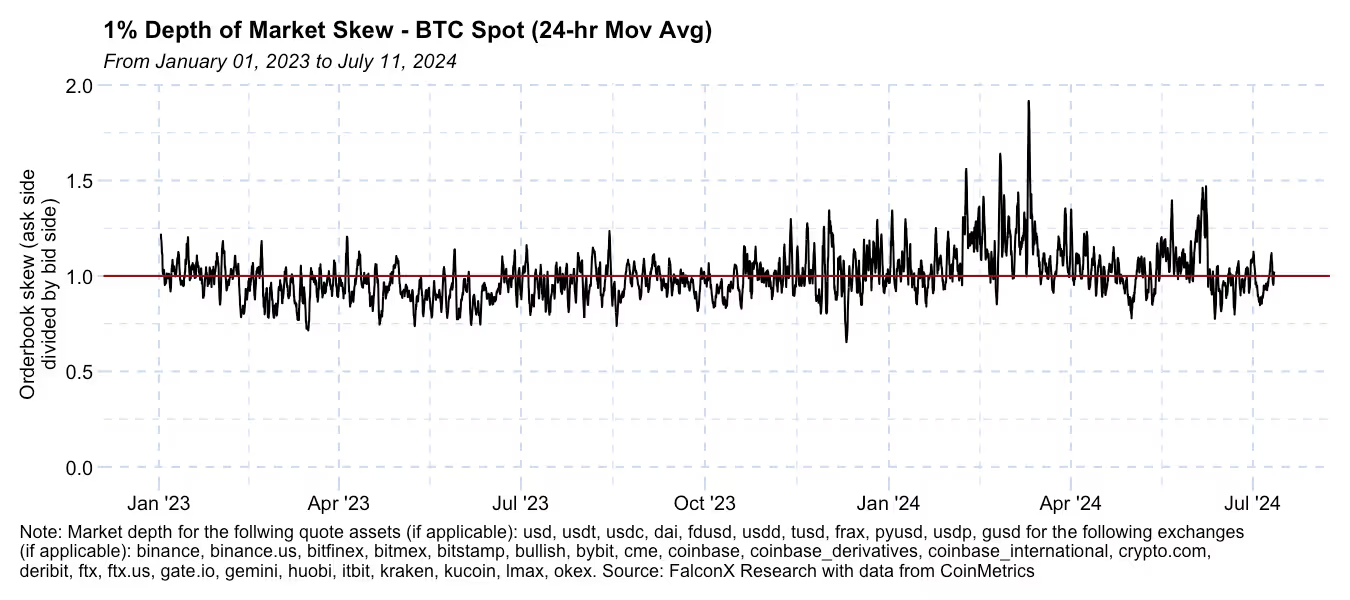

Perhaps a more general way to measure how well the selling pressure was cushioned is orderbook skew. Usually, during strong demand/supply imbalance periods, order books tend to become lopsided. The chart below shows how the 1% orderbook skew (ask side divided by buy side of the book) for the spot BTC market did not drift away from its regular balance this time in July.

There is still more potential supply overhang to hit the market over the upcoming months, and the next focus will be the proceeds related to defunct exchange Mt. Gox. It is unclear what percentage of the 95,000 BTC release (the part of the total 140,000 BTC that chose to receive early distributions in exchange for a 10% haircut) will hit the market.

These sales might have a different profile from the German government sales. For example, maybe more flow will go to exchanges versus professional liquidity providers, or maybe a more diversified holder base will out sales over time.

But the market resilience this week, the prospect of some of the $16.3 billion FTX repayment over the next months translating into buying pressure, the increasingly positive stance toward crypto on both sides of the aisle, and the potential of an interest rate cut in September benefiting risk assets more generally should embolden medium- and long-term bulls.

Other Trends We're Watching

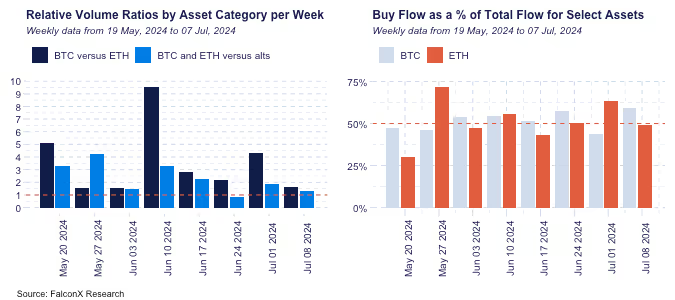

FalconX Trading Desk Color: Flows from most investor personas at our desk have been close to 50/50, with hedge funds and prop desks slightly skewed to the buy side while retail aggregators and venture capital funds primarily on the sell side. ETH volumes have been picking up as our desk's BTC/ETH volume ratio shrunk to its lowest level in almost four months. Alts volume also came in relatively strong, with names such as TON and DOGE attracting buying interest, while SOL and AVAX brought flow in the opposite direction.

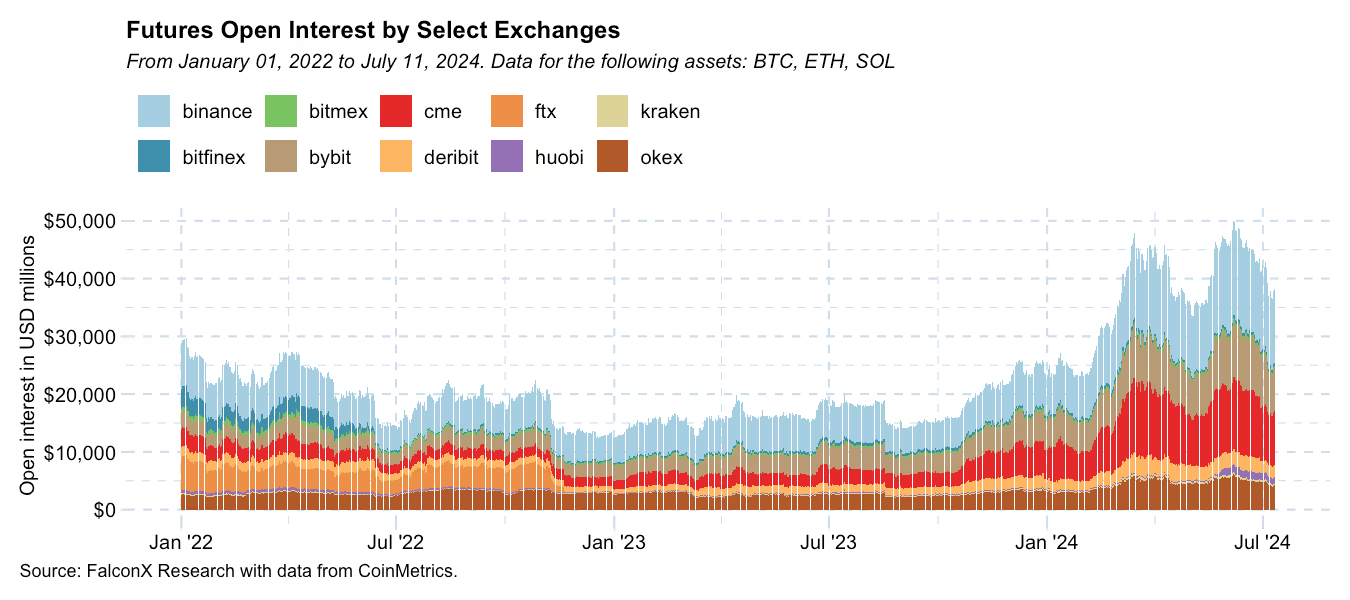

Significant Decline in Futures Open Interest for Larger Names Suggests Some Market Deleveraging: For the first time since May, the combined futures open interest in BTC, ETH, and SOL has fallen below $40 billion, following a peak of $50 billion in June. The decrease was distributed relatively evenly among exchanges and assets, with the CME losing 1% of the market share to Binance and the BTC losing half a percentage point to ETH and SOL.

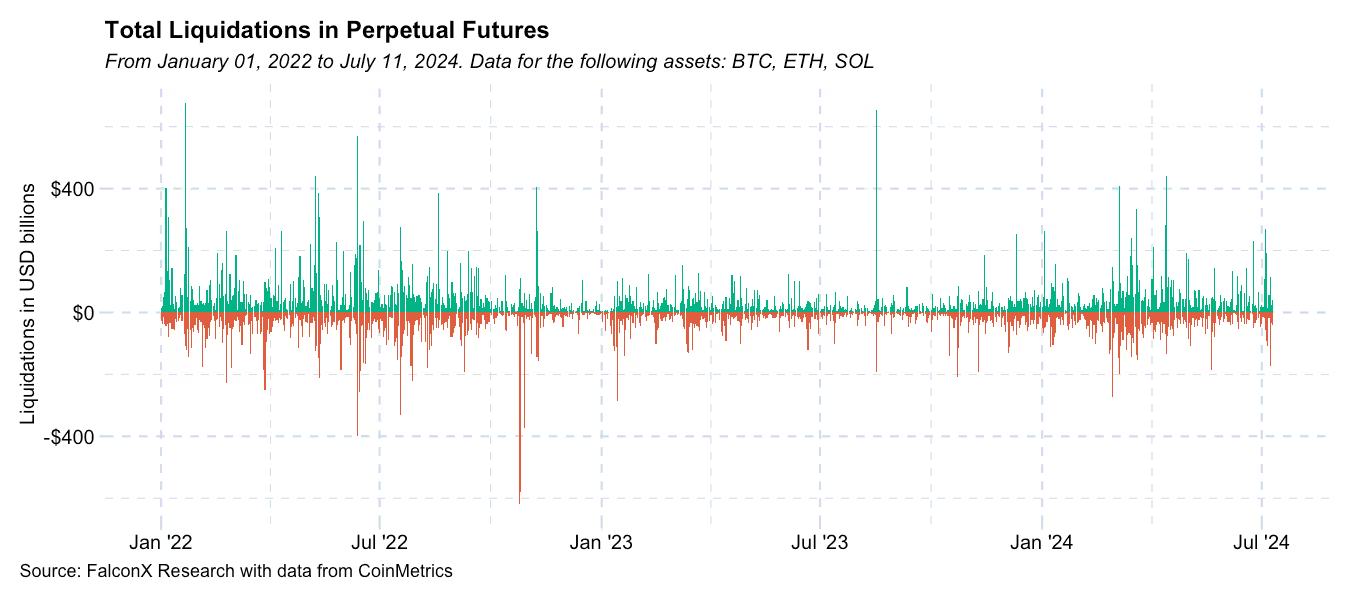

The drop in open interest has been steeper than the 13-17% price drawdown since mid-June, suggesting that the market has somewhat deleveraged. Case in point: liquidations of over $460 million in BTC, ETH, and SOL perpetual futures during the market correction on July 4 and July 5, with July 4 marking the fifth largest liquidation day in 2024.

All this suggests that it will take more to see liquidations in perpetual futures exacerbating price declines like we saw on July 4. The liquidation map estimated by Coinglass, which covers only BTC, indicates that liquidations are now more skewed to shorts and to longs and that BTC could drop $1,000 in price with minimal long liquidations.

Have a great weekend!

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.