Market Rally Broadens; Can SOL Sustain Its Momentum?

The crypto market rally has broadened, with SOL leading the charge, posting a 27.66% gain over the past week and spotlighting its potential as an established asset in the next bull market, supported by developments like Firedancer and DePIN applications. Despite SOL's impressive performance and robust liquidity, its adoption and activity numbers remain modest compared to Ethereum, raising questions about its ability to sustain momentum and break through key price levels.

Market Rally Broadens; Can SOL Sustain Its Momentum?

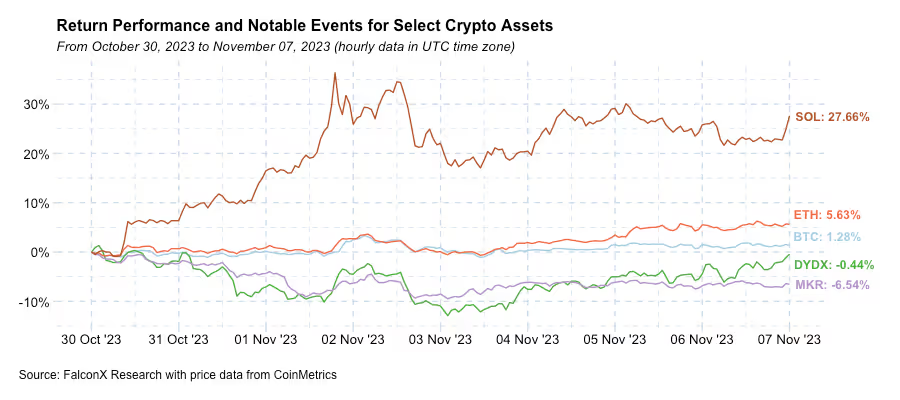

Crypto continues to grind higher, with the rally spreading further into non-BTC assets. The total crypto market cap climbed 5.78% (or 6.40% excluding stablecoins) to $1.3 trillion (or $1.17 trillion excluding stablecoins), the highest level of the year.

ETH had a better week than BTC for the first time in a while due to a combination of BTC spot ETF news flow cooling down and the ETH/BTC price ratio touching multi-year lows (more on that later). Only two names among the main assets posted a negative performance last week (DYDX and MKR), mostly due to corrections from strong recent performances.

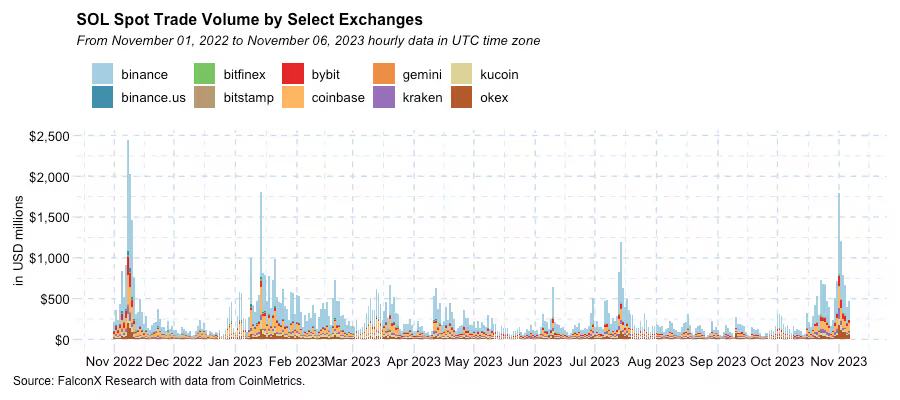

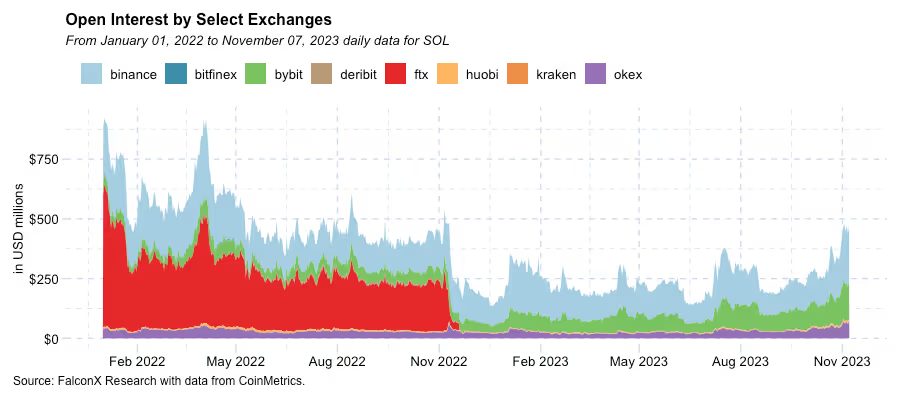

But the real star of the week was SOL, which is now up a whopping 27.66% over the past week and more than 300% so far in 2023. Not only that, but a robust liquidity context marked these prices. As the two charts below show, spot trade daily trade volume reached $1.8 billion, and open interest brushed $500 million, the highest prints since the FTX meltdown.

The rationale behind SOL’s recent rise is that it could graduate to an established asset during the next bull market, somewhat like ETH did in the last. If Bitcoin is the immutable blockchain and Ethereum is the programable blockchain, Solana could earn the spot of the performant blockchain.

In the medium to long terms, I see two main developments supporting this narrative. Firedancer, the high-performance validator software developed by Jump Trading that can make the network faster and more reliable, just launched on testnet. On top of that, one of the leading potential new use cases in crypto, DePIN (decentralized physical infrastructure networks) applications such as Helium, Hivemapper, and Render Network have all launched in or moved to Solana. Add to that Solana’s vibrant community, which was at full display at the ecosystem’s flagship conference Breakpoint last week.

All in, SOL’s market capitalization (fully diluted) of about one-tenth of ETH’s and one-third of XRP’s might not be a steal, but it’s clearly not stretched on a relative basis.

The flip side of that is that all these drivers are prospective.

Current Solana adoption and activity numbers are still modest. According to crypto data provider Artemis, Solana’s total TVL stands at about $430 million, less than 2% of Ethereum’s and lower than Avalanche’s. DEX volumes are showing some traction, but it still stands at only 7% of Ethereum’s and about half of Polygon’s. The total stablecoin market capitalization on Solana amounts to 2% of Ethereum’s and is only 22% and 25% higher than Avalanche’s and Polygon’s, respectively.

The question for SOL to break the $45 price level last seen in August 2022 in the short term is how much the market is willing to discount SOL’s bright prospects. I would not be surprised to see SOL correct a bit or pause to catch its breath before breaking the recent highs.

Other Top Trends We’re Watching

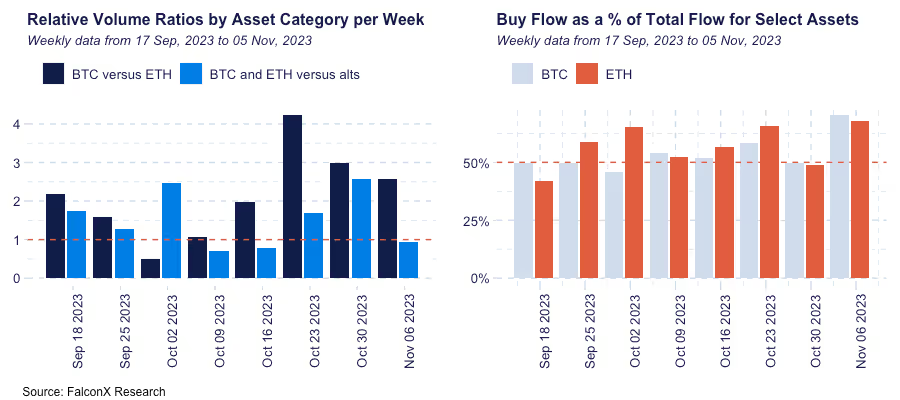

FalconX Trading Desk Color: BTC crossed our desk at 2.6x more than ETH. Notably, however, BTC’s dominance shrunk for the third week in a row. Most investor personas were generally better buyers: Our desk was a better buyer for both BTC (70% of total flow) and ETH (68% of total flow). Alt flows were somewhat subdued, with all alts trading only 0.9x of majors BTC and ETH, the lowest print over the past four weeks. Generally, Buy/Sell ratios across alts did not drift too far away from 50%. The main exceptions were SOL, for which we saw some selling activity during the most acute phase of last week’s rally, and LINK, which continues to attract buying interest.

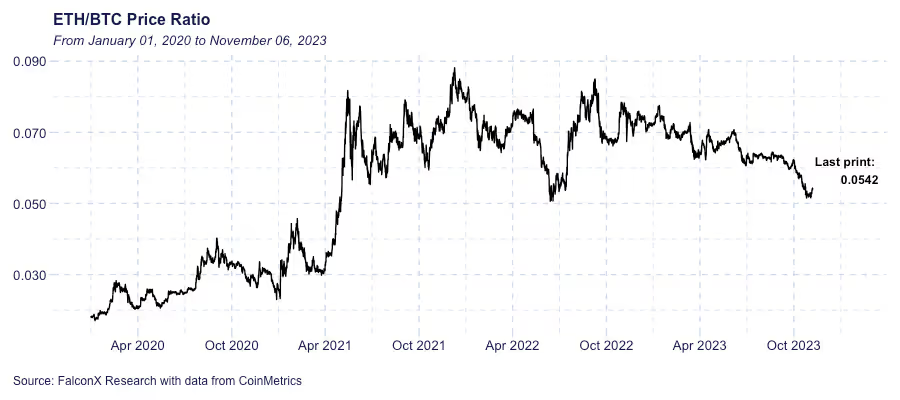

Has the ETH/BTC Ratio Bottomed? Last week was the first time ETH outperformed BTC significantly (about four percentage points) in a long time. Still, the ETH/BTC ratio is only 8% above the lowest level it has been since Q2 2021 (or the time ETH became established as an institutional asset).

Although BTC has much going for it with the likely upcoming spot ETF approval, ETH could have room to outperform in the medium term. The two critical potential triggers would be the next Dencun upgrade, which could come in the first half of 2024, and the emerging narrative of an ETH spot ETF launch.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd. nor Banzai Pipeline Limited service retail counterparties, and the information in this material is NOT intended for retail investors. This material is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this material is not and should not be regarded as investment advice, investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over the counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered as a Swap Dealer with the U.S. Commodities Futures Trading Commission and is a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is licensed by the MFSA as a Class 2 Crypto-Asset Service Provider (Regulation (EU) 2023/1114). It is also licensed as a Financial Institution (Cap. 376) exclusively for EMT payment services.

"FalconX" is a marketing name for the FalconX Group and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.