The Anatomy of the Recent Correction and Why Our Positive Outlook Remains Intact

This correction feels different from the previous one, which occurred right after BTC crossed its previous all-time high price of $69k for the first time. Although the changing macro environment deserves close attention, this is looking just like a typical crypto bull market correction for now.

After brushing the $3 trillion total market cap mark, the crypto market took a nosedive due to a batch of inflation prints coming in worse than expected and clouding the waters of monetary policy projections. The CME FedWatch Tool shows that the odds of a rate cut in May shrunk from 23% a week ago to less than 5% now.

BTC still managed to close the week flat, while ETH was down 5% despite the successful activation of the Dencun upgrade (more on that below). Layer 2 solutions OP and ARB were down double digits as their high-beta ETH characteristics and strong recent price performance weighted more than them being some of the major beneficiaries of the recent Ethereum upgrade. On the bright side, SOL, which is underperforming year-to-date, and MKR, which is raising excitement around its upcoming “endgame” features, managed to clock in double-digit gains.

This correction feels different from the previous one, which occurred right after BTC crossed its previous all-time high price of $69k for the first time.

The previous correction was primarily a leverage washout, with long liquidations in the BTC and ETH perpetual futures market reaching the second-highest level since late 2022. This time, liquidations have so far reached less than half of that amount.

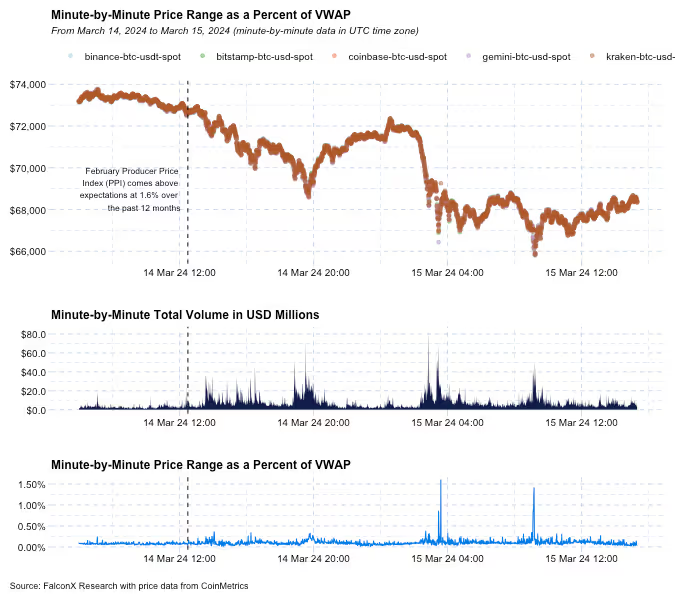

The chart below shows minute-by-minute prices, volumes, and price dispersion for BTC’s main trading pairs. Liquidations are usually characterized by spikes in the bottom chart (price dispersion). Although liquidations have been an accelerant, the market has been heavy since worse-than-expected inflation numbers started to hit the tape.

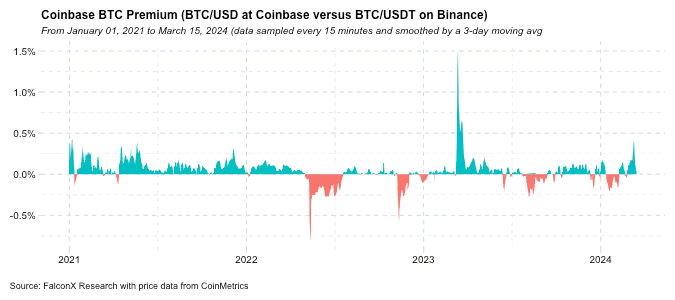

While liquidations hit during Asia hours, there are indications that the correction started in the U.S. market. The Coinbase premium, a gauge of the relative interest from U.S. mainstream retail and ETF issuers, turned negative after reaching its second-highest level of the past three years.

ETF flows yesterday were less than $150 million, a solid showing but significantly below the $744 million average of the three days prior, which did not help. Still, these products recorded a net inflow despite over $250 million of GBTC outflows. Today’s net inflow numbers, which will reflect the overnight correction, could also give us a glimpse of the profile of the recent ETF buyers.

Although the changing macro environment deserves close attention, this is looking just like a typical crypto bull market correction for now.

The outlook for spot BTC inflows remains bright, as most larger platforms are still in the early stages of opening access for their clients.

From a medium-term perspective, two additional factors make me excited.

First, institutional investment managers with discretion over $100 million will file their quarterly 13F forms, which contain the securities they hold, by May 15. This will give us a glimpse into whether there’s any adoption from this corner of the market and could bring positive surprises.

Second, the potential listing of options on BTC spot ETFs over the next months remains a possibility. This could bring in a new wave of inflows.

Other Top Trends We're Watching

Ethereum Dencun Upgrade Activates Smoothly; ETH/BTC Price Ratio Still Attractive: The key feature of the upgrade is introducing a new way to store data on Ethereum through new structures called “blobs.” The new mechanism basically provides an HOV lane for L2 scaling solutions and relief pressure from blockspace on the Ethereum main chain.

The Ethereum network is already posting over 200 blobs per hour (or between one and two per block), with StarkNet, ZKSync, Optimism, and Base starting as the most active L2s, but Arbitrum is catching up quickly. Just a few days after the upgrade, about 0.5% of all Ethereum transactions are already blobs (i.e., type 0x3).

It is still too early to gauge how much cost savings Dencun will bring to L2s, but most market participants have been expecting up to 80-90%. At this early stage, cost savings are even higher, but that is because blobs usage is still expected to pick up from here. The focus over the next few weeks and months will be on where these fees will stabilize.

At any rate, Dencun is a major milestone for the Ethereum ecosystem that will improve the user experience, especially for applications that depend on lower fees and fast transactions.

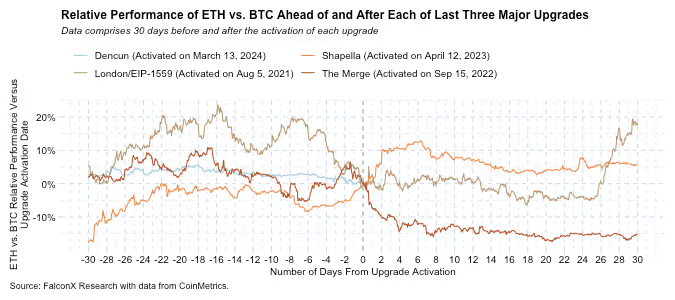

From a price perspective, ETH followed its historical tendency to outperform BTC ahead of key upgrades, as we highlighted previously. But the story starts to get interesting from here on, as after upgrades there’s no defined historical tendency.

I remain bullish on ETH for 2024.

Perhaps some of the recent underperformance can be attributed to some market analysts recently lowering their odds of a spot ETH ETF approval by May 23 to less than 50%, mostly due to a lack of engagement from the SEC. I remain in the 50% camp, though, as I believe many of the wrinkles that were ironed out during the spot BTC ETF approval process do not need to be discussed this time.

Even if the ETF is not approved at this time, ETH does not lack catalysts.

One I’m excited about is the EigenLayer mainnet rollout, which could start soon and lead to launch in the middle of the year. EigenLayer is already the second-largest application in terms of TVL as the introduction of the ability for ETH holders to derive extra yield by helping secure other chains has been building for many months.

In addition, the potential token launch of LayerZero in the summer will lift the interoperability narrative, which is important for networks like Ethereum that are choosing a more modular architecture versus Solana’s monolithic setup.

Although ETH has been outperforming BTC for the past four months, the relative price ratio is only slightly above its lows from mid-2023.

This material is for informational purposes only and is only intended for sophisticated or institutional investors. Neither FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., FalconX Foxtrot Pte Ltd., FalconX Golf Pte Ltd., Solios, Inc., Falcon Labs, Ltd., KestrelX, Ltd., nor Banzai Pipeline Limited (separately and collectively “FalconX”) service retail counterparties, and the information on this website is NOT intended for retail investors. The material published on this website is not (i) an offer, or solicitation of an offer, to invest in, or to buy or sell, any interests or shares, or to participate in any investment or trading strategy, (ii) intended to provide accounting, legal, or tax advice, or investment recommendations, or (iii) an official statement of FalconX or any of its affiliates. Any information contained in this website is not and should not be regarded as investment research, debt research, or derivatives research for the purposes of the rules of the CFTC or any other relevant regulatory body.

Prior to entering into any proposed transaction, recipients should determine, in consultation with their own investment, legal, tax, regulatory, and accounting advisors, the economic risks and merits, as well as the legal, tax, regulatory and accounting characteristics and consequences of the transaction. Pursuant to the Dodd-Frank Act, over-the-counter derivatives are only permitted to be traded by "eligible contract participants" (“ECP”s) as defined under Section 1a(18) of the CEA (7 U.S.C. § 1a(18)). Do not consider derivatives or structured products unless you are an ECP and fully understand and are willing to assume the risks.

Solios, Inc. and FalconX Delta, Inc. are registered as federal money services businesses with FinCEN. FalconX Bravo, Inc. is registered with the U.S. Commodities Futures Trading Commission (CFTC) as a swap dealer and a member of the National Futures Association. FalconX Limited, FalconX Bravo, Inc., FalconX Delta, Inc., Falcon Labs Ltd., and Solios, Inc. are not registered with the Securities & Exchange Commission or the Financial Industry Regulatory Authority. FalconX Golf Pte. Ltd. is not required to be registered or licensed by the Monetary Authority of Singapore (MAS). MAS has granted FalconX Foxtrot Pte. Ltd. a temporary exemption from holding a license under the PSA for the payment services caught under the expanded scope of regulated activities for a specified period. FalconX Limited is a registered Class 3 VFA service provider with the Malta Financial Services Authority under the Virtual Financial Assets Act of 2018. FalconX Limited is licensed to provide the following services to Experienced Investors, Execution of orders on behalf of other persons, Custodian or Nominee Services, and Dealing on own account. FalconX’s complaint policy can be accessed by sending a request to complaints@falconx.io

"FalconX" is a marketing name for FalconX Limited and its affiliates. Availability of products and services is subject to jurisdictional limitations and capabilities of each FalconX entity. For information about which legal entities offer trading products and services, or if you are considering entering into a derivatives transaction, please reach out to your Sales or Trading representative.

.png)